Costs of Caring | AHA

Introduction

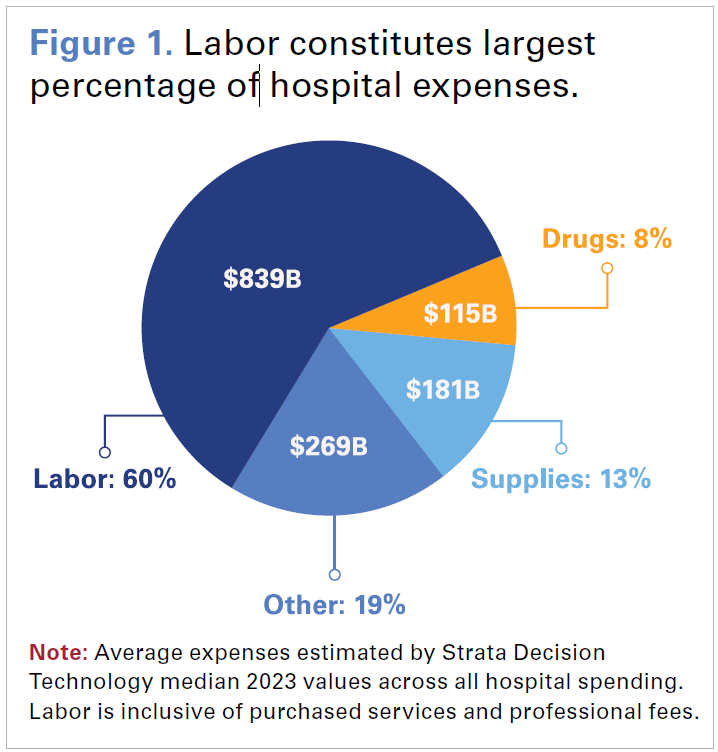

Hospitals and health systems have been at the forefront of a major transformation while at a crossroads of increasing demand for higher acuity care and deepening financial instability. Persistent workforce shortages, severe fractures in the supply chain for drugs and supplies, and high levels of inflation have collectively fueled hospitals’ costs as they care for patients 24/7 (see Figure 1). At the same time, hospitals’ costs have been met with inadequate increases in reimbursement by government payers and increasing administrative burden due to inappropriate commercial health insurer practices.

Hospitals and health systems have been at the forefront of a major transformation while at a crossroads of increasing demand for higher acuity care and deepening financial instability. Persistent workforce shortages, severe fractures in the supply chain for drugs and supplies, and high levels of inflation have collectively fueled hospitals’ costs as they care for patients 24/7 (see Figure 1). At the same time, hospitals’ costs have been met with inadequate increases in reimbursement by government payers and increasing administrative burden due to inappropriate commercial health insurer practices.

Taken together, these issues have created an environment of financial uncertainty where many hospitals and health systems are operating with little to no margin. While recent data suggest that some hospital and health system finances have experienced modest stabilization from historic lows in 2022, the hospital field is still far from where it needs to be to meet the demand for care, invest in new and promising technologies and interventions, and stand ready for the next health care crisis.

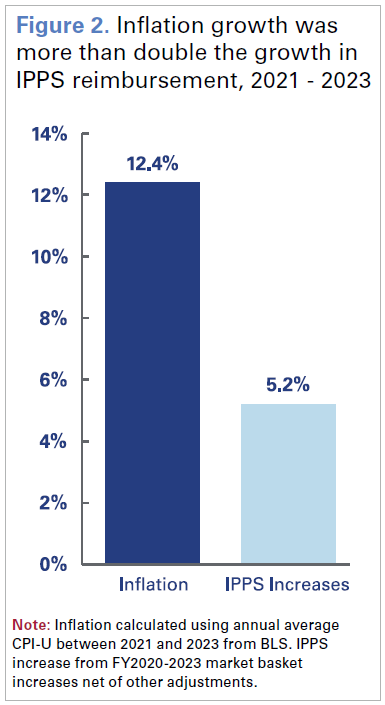

Fresh off a historically challenging year financially in 2022 in which over half of hospitals closed out the year operating at a loss, many hospitals spent much of 2023 simply struggling to break even.1 Economy-wide inflation grew by 12.4% between 2021 and 2023 – more than two times faster than Medicare reimbursement for hospital inpatient care (see Figure 2).

Fresh off a historically challenging year financially in 2022 in which over half of hospitals closed out the year operating at a loss, many hospitals spent much of 2023 simply struggling to break even.1 Economy-wide inflation grew by 12.4% between 2021 and 2023 – more than two times faster than Medicare reimbursement for hospital inpatient care (see Figure 2).

Since the start of 2022, the number of days cash on hand for hospitals and health systems has declined by 28.3%, according to data from Strata Decision Technology, which provides data and cloud-based financial planning, decision support and performance analytics solutions.2

Diverting dollars from their reserves to maintain access to care has required tradeoffs that have limited many hospitals and health systems from investing in updated infrastructure, new medical technology and equipment, and other clinical needs — particularly among those hospitals in severe financial distress.3,4 For example, the average age of capital investments for medical equipment and infrastructure, after years of remaining relatively flat, increased by 7.1% for all hospitals in 2023, according to data from Strata Decision Technology. While the constraints and burdens of increasing plant age present serious challenges to hospitals and health systems in their own right, the inability to make needed capital investments has contributed to bond rating agencies issuing rating downgrades, making it harder for some hospitals and health systems to borrow money.5 Ongoing reimbursement challenges, made worse by crises like the recent Change Healthcare cyberattack, and increased operating costs create an unsustainable financial environment.6 While these challenges alone could cripple any organization, hospitals and health systems continue to face additional threats from ongoing Medicaid redeterminations increasing uncompensated care7, regulatory changes that add operational burden, cyberattacks that threaten the health care infrastructure and potential legislation that would further cut Medicare payments to hospitals.

This report provides a snapshot of the current cost realities facing hospitals and health systems and how they impact their ability to care for patients and communities.

1. Costs of Providing Essential Services

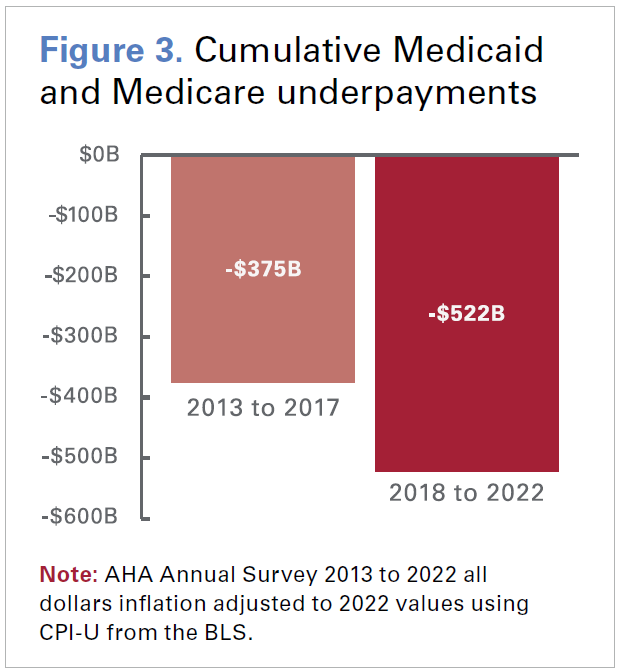

Hospitals often play the critical — and sometimes only — role in providing access to essential health care services, such as emergency care and behavioral health, which are necessary for the health and well-being of the communities they serve. Further, oftentimes these are services that are not offered by other types of health care providers. In 2022, the most recent year for which data are available, hospitals admitted nearly 137 million patients in emergency departments and delivered over 3.5 million babies.8 Many of these essential services are extremely resource intensive and costly to offer. Further compounding this issue are demographic trends such as an aging population and clinical factors such as higher patient acuity. This has driven a steady rise in the share of inpatient utilization among more clinically complex patients covered by Medicare and Medicaid.9 Not only are inpatient services costlier to provide, but public payer payments for these services fall well below costs. In fact, underpayments from Medicare and Medicaid totaled nearly $130 billion in 2022, and Medicare paid just 82 cents for every dollar hospitals spent caring for patients — resulting in a shortfall of almost $100 billion.10 Troublingly, cumulative underpayments in the second half of the last decade totaled more than half a trillion dollars — a nearly 40% increase compared to the first half even after adjusting for inflation (see Figure 3).

Hospitals often play the critical — and sometimes only — role in providing access to essential health care services, such as emergency care and behavioral health, which are necessary for the health and well-being of the communities they serve. Further, oftentimes these are services that are not offered by other types of health care providers. In 2022, the most recent year for which data are available, hospitals admitted nearly 137 million patients in emergency departments and delivered over 3.5 million babies.8 Many of these essential services are extremely resource intensive and costly to offer. Further compounding this issue are demographic trends such as an aging population and clinical factors such as higher patient acuity. This has driven a steady rise in the share of inpatient utilization among more clinically complex patients covered by Medicare and Medicaid.9 Not only are inpatient services costlier to provide, but public payer payments for these services fall well below costs. In fact, underpayments from Medicare and Medicaid totaled nearly $130 billion in 2022, and Medicare paid just 82 cents for every dollar hospitals spent caring for patients — resulting in a shortfall of almost $100 billion.10 Troublingly, cumulative underpayments in the second half of the last decade totaled more than half a trillion dollars — a nearly 40% increase compared to the first half even after adjusting for inflation (see Figure 3).

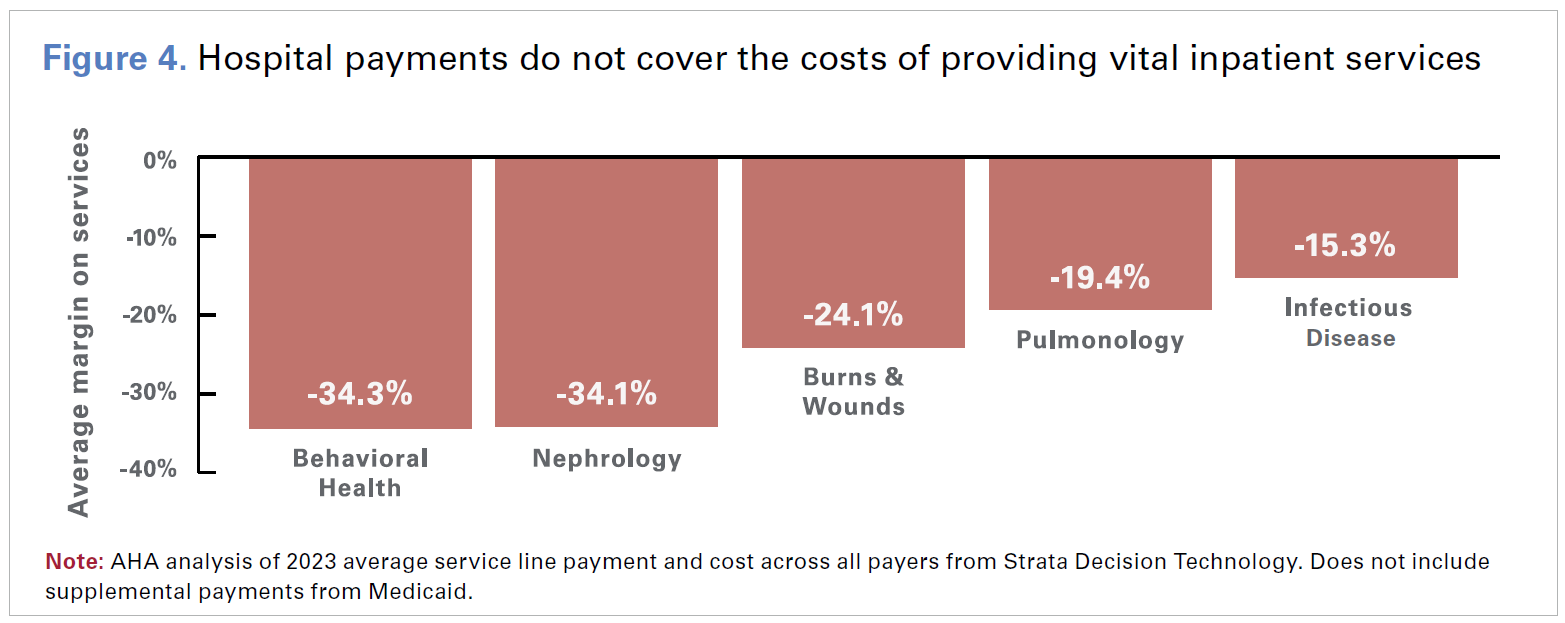

However, the reimbursement challenges do not end with Medicare and Medicaid Reimbursement for some services consistently fall below costs across all payer types. For example, payments for inpatient behavioral health services were 34.3% below costs across all payers on average in 2023, according to data from Strata Decision Technology (see Figure 4). This is especially concerning given the increased utilization of behavioral health services over the last few years.

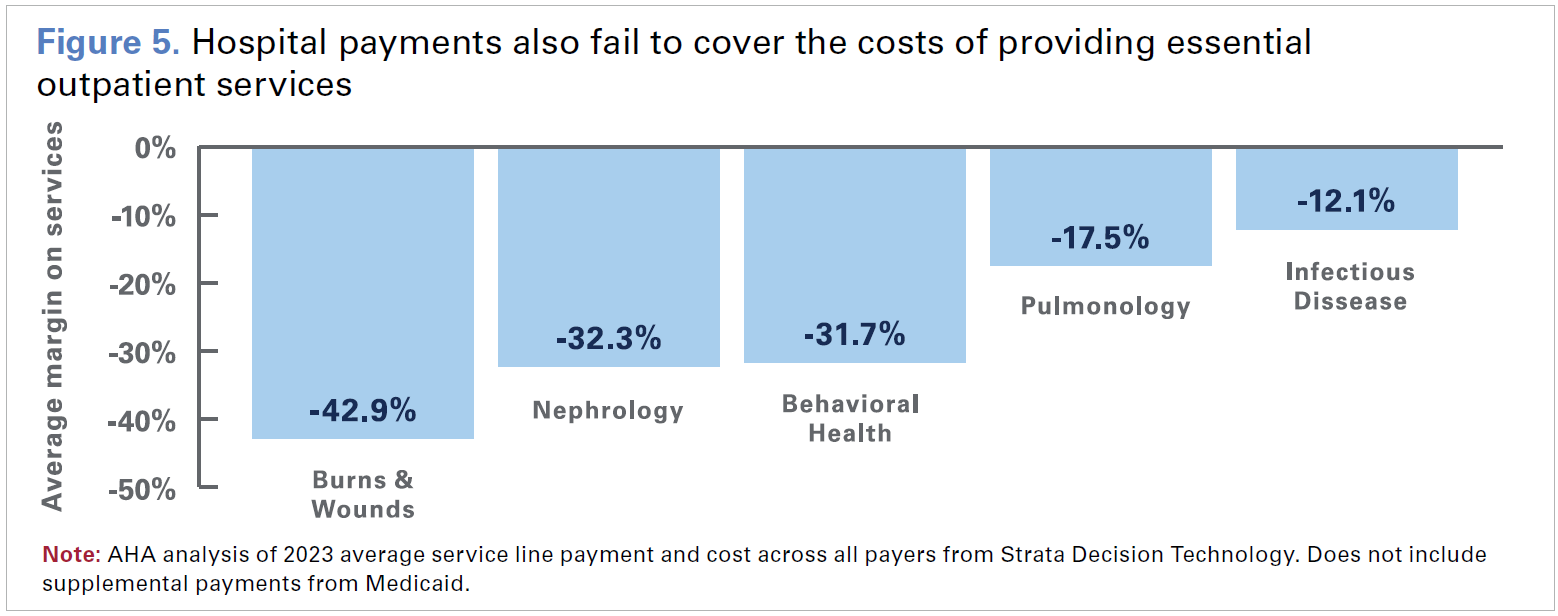

In the outpatient setting, average payments for costly burn and wound services were 42.9% below costs across all payers (see Figure 5). These shortfalls have been especially acute for government payers like Medicare. For example, average Medicare margins for behavioral health services were -38.9% in 2023.

Taken together, these data highlight the challenges that hospitals and health systems face in providing essential services that communities need. This is particularly true for hospitals in rural areas, where the financial challenges can be even more severe.

2. Hospital Administrative Expenses

Some commercial health insurer practices increase hospital costs and delay care to patients

Some commercial health insurer practices increase hospital costs and delay care to patients

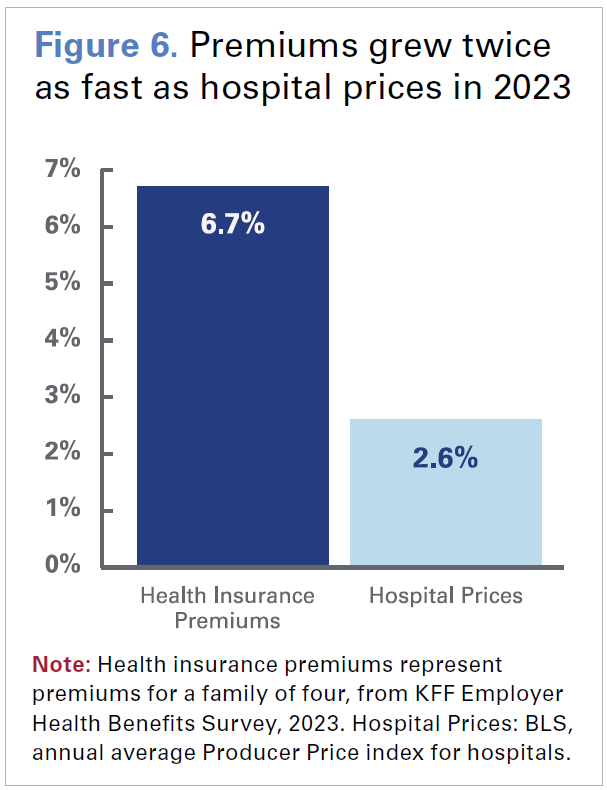

Hospitals have seen significant growth in administrative costs due to inappropriate practices by certain commercial health insurers, including Medicare Advantage (MA) and Medicaid managed care plans. In addition to increasing premiums, which grew twice as fast as hospital prices in 2023, commercial health insurers have overburdened hospitals with time-consuming and labor-intensive practices like automatic claims denials and onerous prior authorization requirements (see Figure 6).11

A 2021 study by McKinsey estimated that hospitals spent $10 billion annually on dealing with insurer prior authorizations.12 Additionally, a 2023 study by Premier found that hospitals are spending just under $20 billion annually in appealing denials — more than half which was wasted on claims that should have been paid out at the time of submission.13 Denials issued by commercial MA plans rose sharply by 55.7% in 2023.14 Notably, many of these denials were ultimately overturned, consistent with a study by the Department of Health and Human Services’ (HHS) Office of Inspector General (OIG) that found 75% of care denials were subsequently overturned.15 These denials are particularly concerning because they often occur for medically necessary care, which can result in direct patient harm. In fact, a recent HHS OIG report found that nearly one in five MA denials met Medicare coverage rules, which meant that had they been paid via Medicare fee-for-service, they would have been paid without denial.16 Even when denials are ultimately overturned, hospitals are not paid for the costs incurred to navigate that burdensome and resource-intensive process. Making matters worse, MA plans paid hospitals less than 90% of Medicare rates despite costing taxpayers more than traditional Medicare in 2023.17,18 Although partly a function of lower rates, the worsening administrative overload is simply costing hospitals more and more.

Though these issues are often felt most acutely with MA and Medicaid managed care plans, it also is true for other commercial payers, where claims denials increased by 20.2% in 2023. Moreover, the time taken by commercial payers to process and pay hospital claims from the date of submission increased by 19.7% in 2023, according to data from the Vitality Index. For hospitals and health systems, these practices result in billions of dollars in lost revenue each year, which require hospitals to divert dollars away from patient care to instead focus on seeking payment from commercial insurers.19 Without further intervention, these trends are expected to continue and worsen. National expenditures on the administrative costs of private health insurance spending alone are projected to account for 7% of total health care spending between 2022 and 2031 and are projected to grow faster than expenditures for hospital care.20

Other expenses

Hospitals also are spending more on things that are not direct patient care services but are still critical to delivering care and maintaining operations. For example, the costs associated with implementing, maintaining and upgrading information management systems and overall technology infrastructure, while critical to improving efficiency and quality of care, typically represent significant investments.

Additionally, given the confidential nature of patient data in these systems, hospitals have increasingly become targets for cyberattacks. As a result, the costs of defending against these attacks and protecting patient data has grown steadily.21 Health care data breaches are by far the costliest of any other sector.22 As cyberattacks and data breaches in health care have grown and regulators are requiring more robust protections, hospitals and health systems are finding themselves increasingly trying to invest in cybersecurity.23 Protecting against cyberattacks and other vulnerabilities is important to patient care, but is increasingly costly. In 2022, hospitals spent nearly $30 billion on property and medical liability insurance, according to data from Lightcast.

3. Hospital Drug Expenses

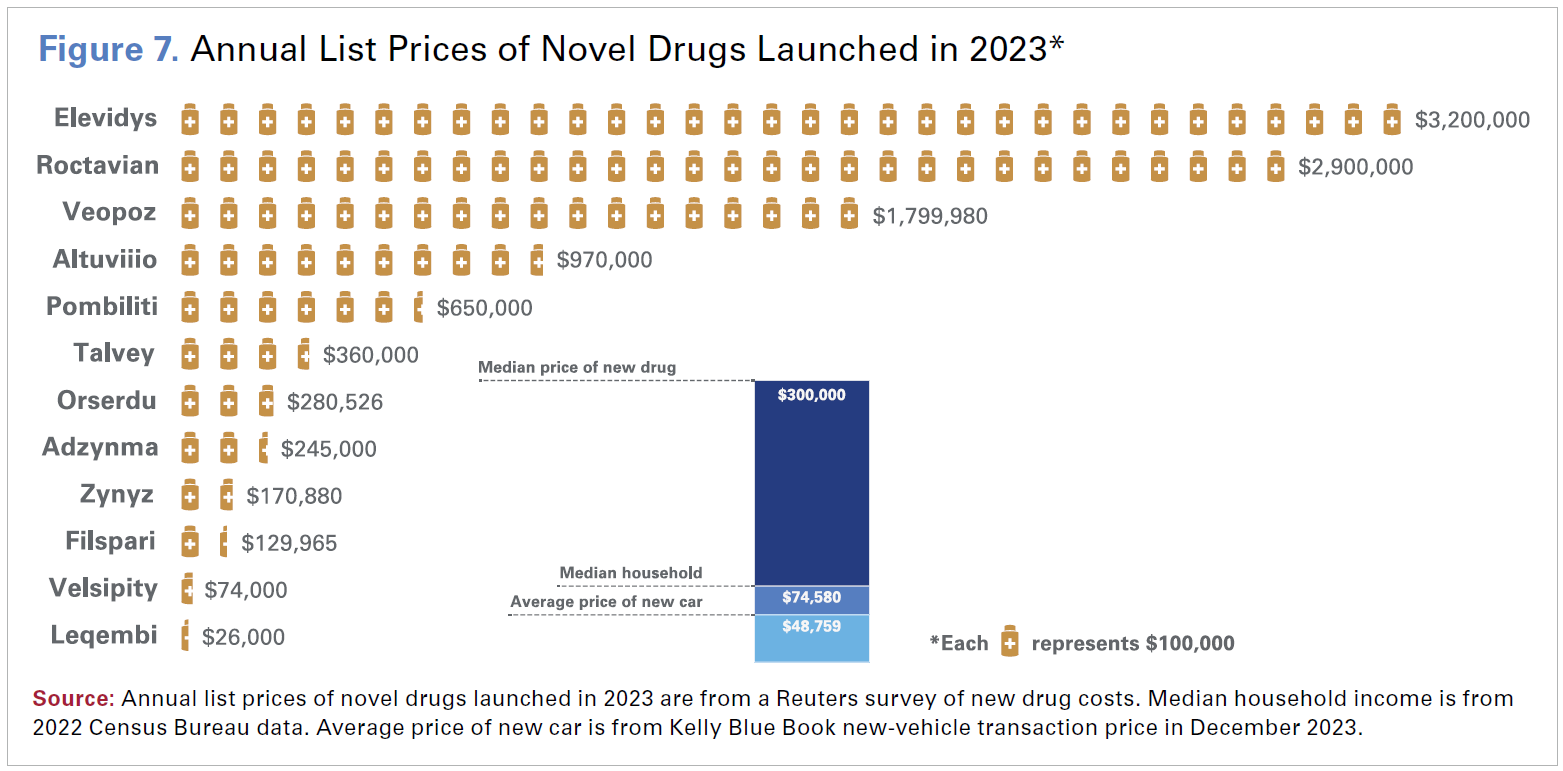

An area of persistent cost pressure for hospitals and health systems has been the rapid and sustained growth in drug expenses. Hospitals spent $115 billion on drug expenses in 2023 alone. One of the factors fueling this growth is drug company decisions to impose large price increases on existing drugs. However, 2023 also saw a continuation of a long-standing trend of drug companies introducing new drugs at record prices. In 2023, the median annual list price for a new drug was $300,000, an increase of 35% from the prior year (see Figure 7).24 A recent report by the HHS Assistant Secretary for Planning and Evaluation (ASPE) found that between 2022 and 2023, prices for nearly 2,000 drugs increased faster than the rate of general inflation, with an average price hike of 15.2%.25

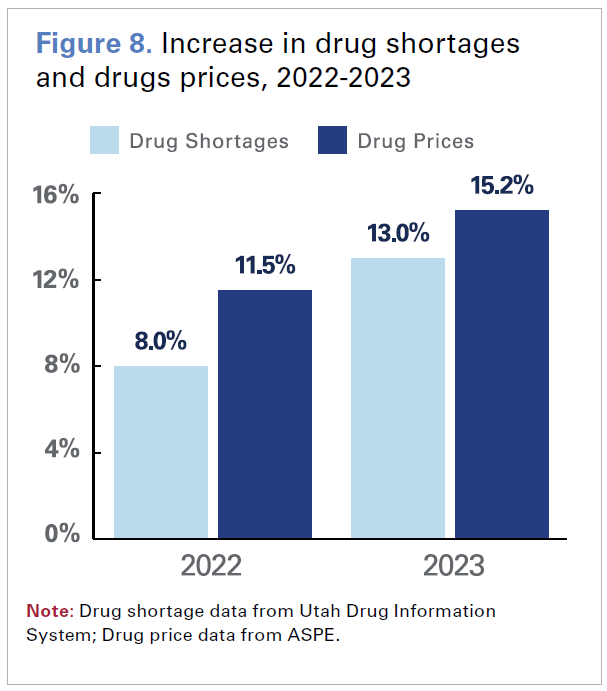

While high drug prices alone pose significant challenges for hospitals and health systems, it is compounded by the fact that many of these same drugs are in shortage. In fact, 2023 saw the most drug shortages in over a decade; there were an average of 301 drugs in shortage per quarter, an increase of 13.0% from the previous year (see Figure 8). These shortages added as much as 20% to hospital drug budgets, according to data from the American Society of Health System Pharmacists (ASHP). These shortages can occur for many reasons, including fractured global supply chains lack of available raw materials, and decisions by drug companies that lack incentives to produce low-margin generic medications.26 An ASHP survey found that more than 99% of hospital and health system pharmacists experienced drug shortages in 2023, with 85% of respondents describing the severity of drug shortages as critically or moderately impactful.27 While generic drugs comprised the majority of medications in shortage, estimated to make up as much as 83% of shortages, many of these drugs also were used to treat cancer and autoimmune diseases.28

While high drug prices alone pose significant challenges for hospitals and health systems, it is compounded by the fact that many of these same drugs are in shortage. In fact, 2023 saw the most drug shortages in over a decade; there were an average of 301 drugs in shortage per quarter, an increase of 13.0% from the previous year (see Figure 8). These shortages added as much as 20% to hospital drug budgets, according to data from the American Society of Health System Pharmacists (ASHP). These shortages can occur for many reasons, including fractured global supply chains lack of available raw materials, and decisions by drug companies that lack incentives to produce low-margin generic medications.26 An ASHP survey found that more than 99% of hospital and health system pharmacists experienced drug shortages in 2023, with 85% of respondents describing the severity of drug shortages as critically or moderately impactful.27 While generic drugs comprised the majority of medications in shortage, estimated to make up as much as 83% of shortages, many of these drugs also were used to treat cancer and autoimmune diseases.28

Hospital pharmacy staff have limited options for navigating drug shortages. They can purchase the drug by going outside their traditional suppliers and group purchasing agreements, access alternate concentrations or package sizes of the drugs than what is needed or purchase a substitute drug with the same clinical indication. However, all three of these options mean hospitals pay higher prices to acquire the drugs. An ASPE report found up to a 16.6% increase in the prices of drugs in shortage; in many cases, the increase in the price of substitute drugs were at least three times higher than the price increase of the drug in shortage.29 The costs incurred as a result of drug shortages are compounded by staff overtime needed to find, procure and administer alternative drugs, to manage the added challenges of multiple medication dispensing automation systems and changing electronic health records (EHRs), and to undergo training to ensure medication safety using alternative therapies.30

4. Hospital Supply Costs

Having adequate and up-to-date medical supplies, devices and equipment are necessary for hospitals to deliver high quality care to patients. These can include artificial joints used to treat patients with conditions such as arthritis, robotic surgery machines used to perform laparoscopic surgical procedures, and complex imaging machinery used for clinical diagnostics. Most of these items are expensive to acquire and maintain and rely on increasingly volatile global supply chains. Comprising approximately 10.5% of the average hospital’s budget, medical supply expenses collectively accounted for $146.9 billion in 2023, an increase of $6.6 billion over 2022, according to data from Strata Decision Technology. As technology and science are constantly evolving, hospitals routinely need to purchase new supplies, devices and equipment that meet clinical care standards and ensure high quality care.

The upfront costs for critical equipment and device upgrades come at a significant cost (Table 1). For example, the advanced technology of cardiac magnetic resonance imaging (cMRI) machines, which have allowed doctors to develop a deeper understanding of cardiac pathologies and has led to improved diagnostics, costs hospitals on average $3.2 million. For some hospitals that have high demand for cardiac services, they may need to purchase multiple cMRI machines. The additional costs for ongoing maintenance, upgrades and staff training also add to the total costs hospitals must incur to deliver their patients with the high quality care.

Table 1. Medical Device and Equipment Market Prices |

| Cutting-edge innovation and technologies provide hospitals with the means to enhance patient outcome in their continuous commitment to delivering top-tier patient care. The featured equipment is intricately connected to advancements in diagnostics, heightened success rates in cardiovascular surgery, and more effective joint replacement procedures. |

| Medical Devices and Equipment | Average List Price |

|---|---|

| Point of Care ultrasound devices | |

| Pocket-sized handheld or tablet-based | $8,143 |

| Compact ultrasound systems* | $73,797 |

| Cardiovascular diagnostic and surgical equipment | |

| Cardiac magnetic resonance imaging (cMRI) machine | $3,230,728 |

| Cardiopulmonary bypass system | $325,442 |

| Joint implant proprietary software and equipment | |

| Image based planning software | $222,132 |

| Navigation software system (guide surgeons in real-time) | $135,365 |

|

*Larger than handheld devices, but still portable. May have more advanced features. Note: Market prices of medical devices and equipment are courtesy of ECRI, an independent not-for-profit corporation that provides a wide range of services dealing with health care technology. |

|

5. Hospital Labor Costs

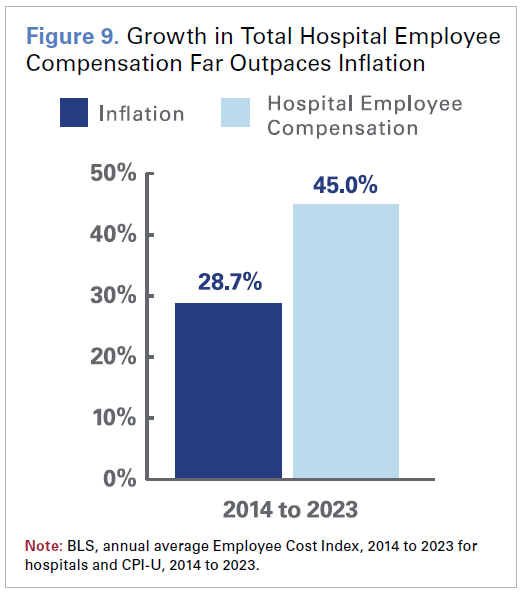

Hospitals’ labor costs increased by more than $42.5 billion between 2021 and 2023 to a total of $839 billion, accounting for nearly 60% of the average hospital’s expenses. Hospitals continue to turn to expensive contract labor to fill gaps and maintain access to care, spending approximately $51.1 billion on contracted staff in 2023.

Though expenditures on contract labor have moderated since pandemic highs, the spending remains elevated and has added to the financial challenges hospitals and health systems face. This is especially true for smaller, rural hospitals where the local workforce pool is smaller and it can be more difficult to recruit staff. Hospitals’ labor costs also can be very sensitive to sudden fluctuations in the demand and supply of labor. Growth in wages and benefits of hospital employees has vastly surpassed economy-wide inflation over the last decade (see Figure 9).

Though expenditures on contract labor have moderated since pandemic highs, the spending remains elevated and has added to the financial challenges hospitals and health systems face. This is especially true for smaller, rural hospitals where the local workforce pool is smaller and it can be more difficult to recruit staff. Hospitals’ labor costs also can be very sensitive to sudden fluctuations in the demand and supply of labor. Growth in wages and benefits of hospital employees has vastly surpassed economy-wide inflation over the last decade (see Figure 9).

Yet, critical labor shortages persist, especially in the face of growing burnout among clinicians. Employee burnout hastened by the pandemic and further exacerbated by commercial insurer administrative burden and increase in violence against hospital employees, led to an unprecedented exodus of health care professionals in recent years.31 Resignations per month among health care workers grew 50% between 2020 and 2023, according to data from McKinsey.32 Additionally, hospitals have been forced to contend with record high turnover rates — fueling additional expenses for hospitals looking to recruit new workers.33

Consequently, hospitals and health systems have invested more to attract and retain talent. Data from Lightcast indicates that advertised wage rates across all hospital jobs jumped by 10.1% during 2023. With a growing gap between supply and demand for health care workers over the next decade, labor costs will likely continue to be an issue for hospitals.

A Look Ahead to the Rest of 2024

Though 2024 is the first full year out of the most recent public health emergency period, hospitals and health systems continue to face many challenges. Credit ratings agencies have painted a bleak picture for the hospital sector in 2024.34 According to the S&P, negative outlooks for not-for-profit hospitals are proportionally at their highest in over a decade, affecting 24% of the sector.35 Similarly, Fitch reported a credit downgrade-to-upgrade ratio of 3:1 — alarmingly close to the ratio seen during the 2008 financial crisis — calling it a “make or break” year and highlighting the sector’s struggles, particularly among smaller hospitals with annual revenues under $500 million.36 While it is expected that hospitals and health systems will continue to face cost increases for labor, drugs, and medical supplies, there are additional headwinds to consider which include:

- Coverage losses due to Medicaid redeterminations: More than 19 million Medicaid enrollees have been disenrolled through 2023.37 Though partially offset by record Marketplace enrollment and possible enrollment in employer-sponsored coverage, this has still resulted in a steady increase in uncompensated care costs throughout 2023 and will likely continue into 2024 – particularly for states that have not expanded Medicaid.38

- Potential legislative actions to cut hospital Medicare payments for patient care: Congress is considering several bills that would impose additional payment reductions to services provided in hospital outpatient departments. These proposals, referred to as “siteneutral” payment cuts, would exacerbate financial challenges for hospitals and threaten patients’ access to quality care.

- Cybersecurity risks impact providers and patient care: The cyberattack on Change Healthcare in February 2024 has underscored the extensive repercussions such incidents can have on patient care and hospital operations. The disruptions stemming from that cyberattack have significantly hindered revenue cycle management, pharmacy services, select health care technologies, clinical authorizations, and more across multiple health systems, serving as an example of how an attack can reverberate across the entire health care sector when a business that provides numerous mission-critical services is compromised.39

- Ongoing and escalating hospital violence: There has been a significant uptick in violence against health care workers in recent years.40 To address this issue, hospitals are making significant investments in violence prevention and preparedness efforts to support their employees.

Conclusion

America’s hospitals and health systems are dedicated to providing high-quality 24/7 care to all patients in every community across the country. While the commitment to caring and advancing health never wavers, hospitals continue to face significant challenges making it difficult to ensure the care is always there.

The AHA continues to urge Congress and the Administration to support policies to make sure hospitals and health systems have the resources they need to continue providing 24/7 care to all patients and communities. These include:

- Rejecting Medicare and Medicaid cuts to hospital care, including harmful site-neutral proposals and forthcoming reductions to Medicaid Disproportionate Share hospitals.

- Supporting and strengthening the health care workforce.

- Protecting the 340B Drug Pricing Program from any harmful changes and reining in the increasing costs of drugs.

- Taking actions to hold commercial insurers accountable for practices that delay, deny and disrupt care.

- Bolstering support to enhance cybersecurity of hospitals and the entire health care system.

End Notes

- www.kaufmanhall.com/news/2022-worst-financial-year-hospitals-and-health-systems-start-pandemic

- www.syntellis.com/sites/default/files/2023-11/aha_q2_2023_v2.pdf

- fortune.com/well/2024/01/11/rural-hospitals-are-caught-in-an-aging-infrastructure-conundrum/

- www.aha.org/guidesreports/2023-04-19-essential-role-financial-reserves-not-profit-healthcare

- www.modernhealthcare.com/finance/hospital-2023-credit-rating-downgrade-fitch-ratings-sp-global-moodys

- www.aha.org/cybersecurity/change-healthcare-cyberattack-updates

- www.aha.org/news/blog/2023-09-20-unwise-dsh-cuts-combined-rise-uncompensated-care-due-medicaid-redeterminations-coverage-losses-further

- AHA analysis of 2022 Annual Survey data.

- www.trillianthealth.com/insights/the-compass/the-total-available-market-of-commercially-insured-patients-is-shrinking

- www.aha.org/news/headline/2024-01-10-aha-infographic-medicare-underpayments-hospitals-nearly-100-billion-2022#:~:text=AHA%20infographic% 3A%20Medicare%20underpayments%20to%20hospitals%20nearly%20%24100%20billion%20in%202022,-Jan%2010%2C%202024&text=Medicare%20 paid%20hospitals%20a%20record,negative%20Medicare%20margins%20that%20year.

- www.wsj.com/health/healthcare/health-insurance-cost-increase-5b35ead7

- www.mckinsey.com/~/media/mckinsey/industries/healthcare%20systems%20and%20services/our%20insights/administrative%20simplification%20 how%20to%20save%20a%20quarter%20trillion%20dollars%20in%20us%20healthcare/administrative-simplification-how-to-save-a-quarter-trillion-dollars- in-us-healthcare.pdf?shouldIndex=false

- premierinc.com/newsroom/blog/trend-alert-private-payers-retain-profits-by-refusing-or-delaying-legitimate-medical-claims

- www.syntellis.com/sites/default/files/2023-11/aha_q2_2023_v2.pdf

- oig.hhs.gov/oei/reports/OEI-09-19-00350.pdf

- oig.hhs.gov/oei/reports/OEI-09-18-00260.pdf

- www.ensemblehp.com/blog/the-real-cost-of-medicare-advantage-plan-success/

- www.medpac.gov/wp-content/uploads/import_data/scrape_files/docs/default-source/reports/mar21_medpac_report_to_the_congress_sec.pdf#page=401

- www.ama-assn.org/practice-management/prior-authorization/health-systems-plagued-payer-takeback-schemes-110000#:~:- text=authorization’s%20 financial%20impact-,Prior%20authorization’s%20financial%20impact,an%20increase%20of%2067%25.%E2%80%9D

- AHA analysis of NHE projections of 2022-2031 expenditures.

- www.healthcaredive.com/news/healthcare-ransomware-costs-comparitech-77-billion/698044/

- intraprisehealth.com/the-cost-of-cyberattacks-in-healthcare/

- www.healthcareitnews.com/news/cisos-face-budgetary-pressures-burnout-during-global-recession

- www.reuters.com/business/healthcare-pharmaceuticals/prices-new-us-drugs-rose-35-2023-more-than-previous-year-2024-02- 23/?utm_source=facebook& utm_medium=news_tab

- aspe.hhs.gov/reports/changes-list-prices-prescription-drugs

- www.fda.gov/media/131130/download?attachment

- news.ashp.org/-/media/assets/drug-shortages/docs/ASHP-2023-Drug-Shortages-Survey-Report.pdf

- www.iqvia.com/insights/the-iqvia-institute/reports-and-publications/reports/drug-shortages-in-the-us-2023?utm_campaign=2023_ Drug_Shortages_Report_ INSTITUTE_IS&utm_medium=email&utm_source=Eloqua

- aspe.hhs.gov/reports/drug-shortages-impacts-consumer-costs

- link.springer.com/article/10.1007/s13181-023-00950-6#:~:text=Shortages%20compromise%20or%20delay%20medical,morbidity%20%5B1%2C%202%5D.

- www.aha.org/system/files/media/file/2023/06/fact-sheet-examining-the-real-factors-driving-physician-practice-acquisition.pdf

- www.mckinsey.com/industries/healthcare/our-insights/how-health-systems-and-educators-can-work-to-close-the-talent-gap

- www.healthcarefinancenews.com/news/rn-turnover-healthcare-rise

- on24static.akamaized.net/event/44/67/84/2/rt/1/documents/resourceList1709062595167/ushealthcaresectorcreditbeat227241709062595167.pdf

- www.spglobal.com/ratings/en/research/articles/231206-historical-peak-of-negative-outlooks-signals-challenges-remain-for-u-s-not- for-profit-acutehealth- care-provi-12927513

- www.fitchratings.com/research/us-public-finance/us-not-for-profit-hospitals-health-systems-outlook-2024-05-12-2023

- ww.kff.org/report-section/medicaid-enrollment-and-unwinding-tracker-overview/

- www.aha.org/news/blog/2023-09-20-unwise-dsh-cuts-combined-rise-uncompensated-care-due-medicaid-redeterminations-coverage-losses-further

- www.aha.org/2024-02-24-update-unitedhealth-groups-change-healthcares-continued-cyberattack-impacting-health-care-providers

- apnews.com/article/hospitals-workplace-violence-shootings-aa6918569ff8f76ff8a15b9813e31686

link